What is Cost Segregation? The Complete Guide

Published: February 8, 2026 | Updated: February 12, 2026

If you are asking what is cost segregation, you are asking how a building’s cost is separated into asset classes with shorter recovery periods under US tax rules. The goal is not a new deduction, but a timing change that accelerates depreciation into earlier years. Investors use it when timing matters for cash flow, hold period strategy, or bonus depreciation windows. This guide frames the concept in operational terms so you can evaluate it with real project facts.

Cost segregation is implemented through an engineering based study that identifies components that qualify as personal property or land improvements. The output is a defensible classification schedule that must reconcile back to the property’s depreciable basis and placed in service timing. The economics depend on tax rate, ability to use losses, and future income expectations. Understanding those constraints upfront prevents unrealistic underwriting.

TL;DR - Key Takeaway

What is Cost Segregation

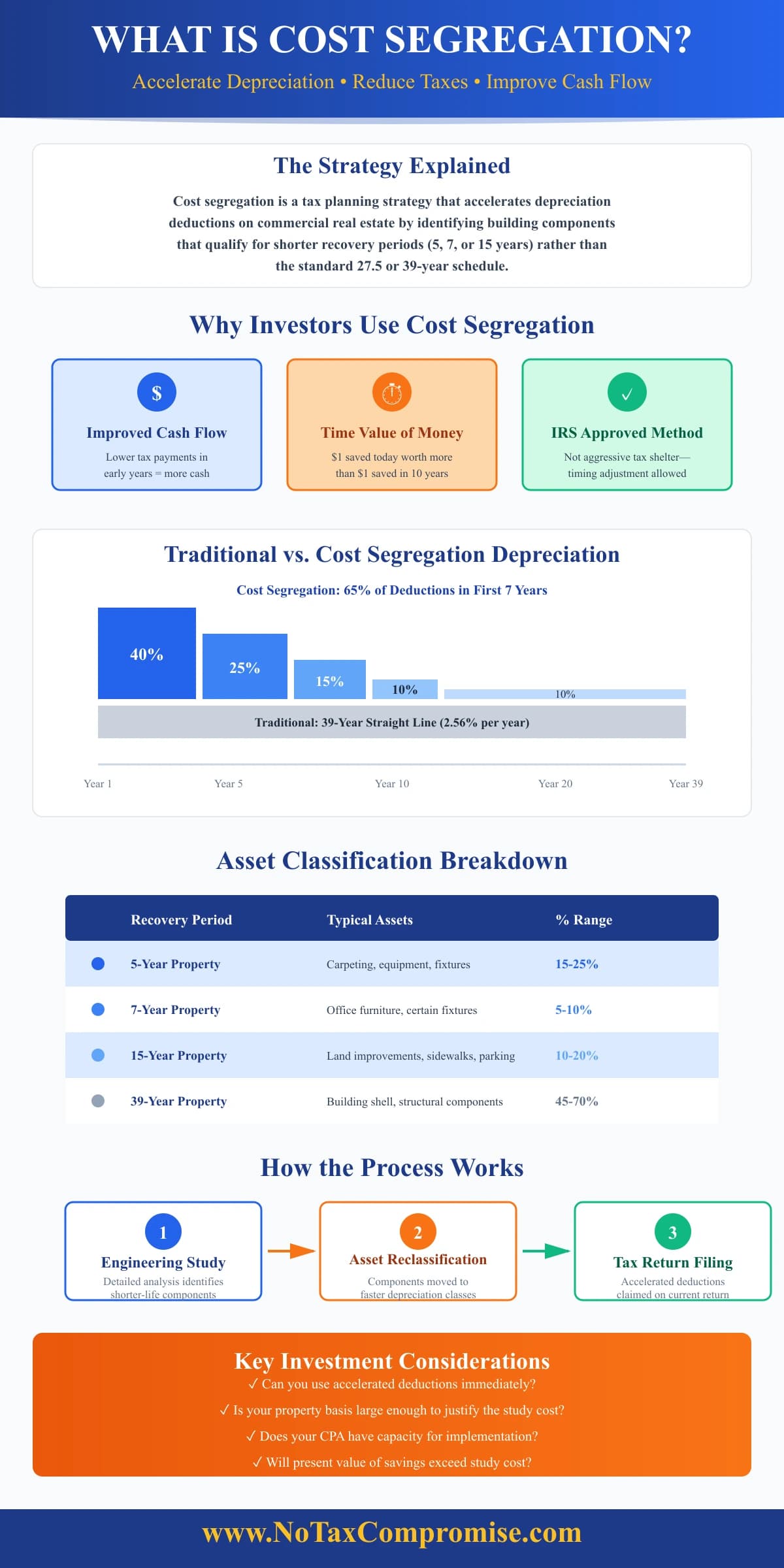

Cost segregation is a tax planning strategy that accelerates depreciation deductions on commercial real estate and income producing properties. The process identifies building components and land improvements that qualify for shorter recovery periods—typically 5, 7, or 15 years—rather than the standard 27.5 or 39-year schedule required for the building structure. By reclassifying these assets into faster depreciation categories, property owners can reduce current taxable income and improve cash flow during the critical early years of ownership.

The strategy works through a detailed engineering analysis that separates a property's depreciable basis from real property into personal property or land improvements. This is not a new tax deduction or aggressive tax shelter—it is a timing adjustment permitted under IRS guidelines and established through decades of case law. The total amount of depreciation claimed over the life of the asset remains unchanged, but cost segregation shifts a larger percentage of deductions into years when they deliver greater financial value to the property owner.

For a high level orientation and the full cost segregation topic map, start with the cost segregation hub. This page stays narrow on cost segregation, what a study produces, and how investors evaluate the decision.

Why Investors Use It

Investors pursue cost segregation primarily for improved cash flow and tax planning flexibility. Accelerating depreciation deductions into earlier years reduces current taxable income, which translates to lower tax payments and increased after tax cash flow during the property's initial holding period. For investors with active income or passive loss limitations, the ability to time when deductions are recognized can determine whether benefits are realized immediately or deferred to future years.

The strategy functions as a timing optimization rather than a permanent tax reduction. Total depreciation over the property's life remains the same, but cost segregation shifts larger deductions forward and smaller deductions to later years. This front loading creates value through the time value of money—a dollar saved in year one has greater present value than the same dollar saved in year ten. The economic benefit depends on the investor's current tax rate, ability to use losses immediately, and expected changes in tax rates or income over the holding period.

Evaluating Cost Segregation: Key Considerations

- Reclassification Potential: What percentage of the property's depreciable basis can reasonably be reclassified into shorter recovery periods based on asset composition?

- Tax Position: Can you utilize accelerated deductions immediately, or will passive loss limitations or insufficient income defer the benefit?

- Implementation Timing: Does your CPA have capacity to incorporate the study into the current tax filing cycle, or should it be coordinated with the next return?

- Cost Benefit Analysis: Will the present value of accelerated tax savings exceed the cost of the engineering based study and ongoing compliance requirements?

Cost segregation is most effective when evaluated as both a technical classification exercise and a financial planning decision. The engineering analysis identifies what can be reclassified, but the investor's tax profile, holding strategy, and cash flow needs determine whether that reclassification creates material value. Understanding both dimensions prevents pursuing studies that may be technically feasible but economically marginal for a specific ownership scenario.

Depreciation Lives and Asset Classes

The mechanism behind cost segregation is depreciation classification. Most building basis is depreciated over 27.5 years for residential rental property or 39 years for nonresidential property. A cost segregation study identifies components that may qualify as shorter life property, often 5 year, 7 year, or 15 year classes, based on facts and classification rules.

Table 1: Typical Buckets in a Cost Segregation Study

| Bucket | Common Items | Investor Relevance |

|---|---|---|

| Short life components | Dedicated electrical, specialty plumbing, certain finishes tied to specific functions | Faster depreciation can increase near term deductions |

| Land improvements | Paving, parking lots, sidewalks, landscaping, exterior lighting | Often recoverable faster than the building shell |

| Building shell | Structural components and major building systems | Remains on the standard recovery period |

Investors sometimes ask about cost segregation and then immediately ask how does cost segregation work. The next article explains the step by step cost segregation process, including the scoping, modeling, and implementation steps that affect outcomes.

What a Cost Segregation Study Delivers

A cost segregation study is the deliverable that turns the abstract concept of cost segregation into a property specific classification schedule. A well built report is designed to be implemented on the tax return and supported if the positions are reviewed.

What a strong report includes

- Asset schedules by recovery period with clear descriptions.

- Methodology narrative describing assumptions and cost estimation approach.

- Reconciliation to total depreciable basis used for depreciation.

- Supporting workpapers, photos, and calculations as applicable.

In practical terms, cost segregation meaning is operational. It is not enough for a report to show a reclassification. It must also reconcile to the basis used on the return and be consistent with how your CPA will book assets and depreciation.

How It Changes Taxable Income

From a tax return perspective, cost segregation is a change in the depreciation schedule. Reclassification can increase depreciation deductions earlier and reduce them later. Because it is often a timing strategy, the economic benefit comes from the time value of money and reinvestment opportunities, not from creating new basis.

Questions to ask before relying on estimates

- Will losses be usable given passive activity and at risk constraints?

- Is the placed in service timing aligned with the tax year being filed?

- Does the model consider your intended hold period and exit timing?

This is why cost segregation explained as a single number can mislead. A useful model shows assumptions and includes scenario ranges.

Decision Criteria and Constraints

A practical investor approach to cost segregation is a decision checklist. The goal is to decide whether the property has enough eligible components and whether the investor can use deductions in a way that justifies the cost and effort.

Table 2: Investor Checklist

| Decision Point | Why It Matters | Practical Action |

|---|---|---|

| Basis and scope are defined | Misstated basis creates reconciliation issues and unreliable outputs. | Confirm basis inputs with your CPA before modeling. |

| Deductions are usable | Loss limitations can delay benefits and change realized economics. | Model usability and timing with your CPA. |

| Data quality supports defensibility | Weak support increases uncertainty and audit defensibility risk. | Gather docs early and keep assumptions explicit. |

If you want to see how these inputs show up in schedules, the examples article provides cost segregation examples with common scenarios. Seeing examples helps clarify cost segregation in practical modeling terms.

Documentation and Defensibility

Documentation is central to defensibility. A cost segregation study should show how components were identified, how costs were determined, and how the totals reconcile to the basis used for depreciation. This is also where cost segregation becomes a compliance discipline rather than a headline estimate.

Defensibility habits

- Keep the final report, inputs, and reconciliations together.

- Document assumptions when invoices or detail are missing.

- Coordinate with the CPA so implementation matches the report.

In summary, cost segregation is a recognized depreciation classification method. It can improve near term cash flow, but realized value depends on eligibility, usability of deductions, and the quality of documentation and implementation.

Frequently Asked Questions

What is cost segregation in one sentence?

Cost segregation is a method that separates building related costs into components so eligible parts can be depreciated faster than the building shell, accelerating deductions into earlier years.

Is cost segregation only for large commercial buildings?

No. Cost segregation is used across property types, including residential rental and commercial real estate. Practical viability depends on depreciable basis, component mix, and whether the owner can use the deductions.

What is cost segregation compared with a standard 27.5 or 39 year schedule?

Standard depreciation generally keeps most basis in the building life. Cost segregation identifies portions that may qualify for shorter recovery periods, which changes the timing of depreciation deductions.

Can cost segregation be done after a property is already placed in service?

Yes. Investors may apply cost segregation after placed in service, but implementation details matter. Your CPA typically determines the appropriate filing approach and how catch up depreciation is handled.

Does cost segregation always create net tax savings over the full holding period?

Not necessarily. Cost segregation is often a timing strategy, so the economic value depends on time value of money, reinvestment, holding period, and the tax consequences at exit, including potential recapture.

What documentation makes a cost segregation study more defensible?

Defensibility improves when the report shows clear methodology, reconciles to basis, documents assumptions, and includes support such as photos, cost detail, and workpapers that explain classification decisions.

Does cost segregation increase audit risk?

Cost segregation does not automatically increase audit risk, but aggressive classification and weak documentation can. A consistent, well supported study reduces defensibility risk.

What is the biggest investor mistake when evaluating what is cost segregation?

The most common mistake is treating a generic percentage estimate as a decision. Investors get better outcomes when they model usability of deductions, timing, and implementation constraints with their CPA.